I need help in explaining the commercial viability of this potential Tantalum lab test result from Africa.

$\begingroup$

$\endgroup$

2

-

$\begingroup$ If you are involved in assessing actual mining potential, perhaps finding an expert consultant would be best in such circumstances, as places like stackexchange may be tougher to get input and less reliable. Googling found responsiblemineralsinitiative.org/training/consultancy-firms but there may be others. $\endgroup$– JeopardyTempestCommented Sep 20, 2021 at 3:34

-

$\begingroup$ Is this commercially viable? Maybe. If you had a mountain of exactly this stuff, it would be great and you would probably be a multi-millionaire. But it's unlikely that you have a mountain of exactly this, so you probably need professional advice from people who know what they're doing. I suggest contacting the government geological survey of the country in which the deposit is located. If no such authority exists, maybe try the Egyptian, Namibian, or South African surveys. $\endgroup$– GimelistCommented Sep 23, 2021 at 1:33

Add a comment

|

2 Answers

$\begingroup$

$\endgroup$

One lab result does not an orebody make.

In terms of economic potential nothing can be ascertained from data in the question.

When it comes to minerals and economics there are two terms that need to known and most people don't realize the difference.

A mineral resource is simply a deposit of a particular mineral, usually associated with a particular metal or metals, or other geological commodity, such as diamonds. No economic significance is attached to a resource.

An reserve is a resource (mineral deposit), or part of a resource, that has been fully and competently assessed and evaluated by geologists and mining engineers and deemed to be economic. It can be mined for a profit.

Additionally, the terms ore and orebody only apply to geological reserves - those parts of a mineral deposit that are economic to mine. If there is no evaluation proving economic viability or an evaluation proves a body/deposit is uneconomic it cannot be called an orebody, or referred to as ore. It's just a deposit of mineralization. Should the price for the commodity increase in the future an additional evaluation, then, might result in it being reclassified as a reserve an hence and orebody.

Any evaluation of a mineral deposit must consider:

- the style of mineralization, the size of the resource, its shape, orientation (whether it is nearly flat or nearly vertical - its dip),

- its true thickness (perpendicular to the dip) as opposed to apparent thickness,

- whether it is one large deposit or a number of smaller deposits and their proximity to each other,

- whether there are differences between proximal deposits,

- the amount of a particular metal or metals, or diamonds or other commodity,

- the mining method or methods to be used,

- the amount of material that can be mined from the deposit (mining recovery),

- the competency of the orebody and surrounding host rock and its implication for ground conditions, mining method and safety,

- the presence and quantities of gangue minerals and deleterious minerals (such as very minor or nuisance amounts of radioactive metals in a copper deposit, or copper in a gold deposit - minerals that could affect the metallurgical recovery),

- proximity to a mineral processing plant for that style of mineralization,

- the amount of minerals and thus metals that can be extracted by the processing plant (processing or metallurgical recovery),

- disposal of waste mineralization and eventual site rehabilitation.

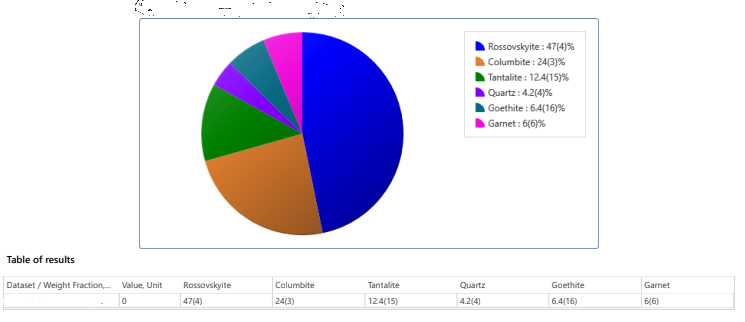

The information presented in the question is simply an overall tabulation of minerals and the proportion of each mineral. There is no indication whether the data is for one sample or one deposit or one site. It does not specify the amount of each specific metal of interest there is in the sample, or deposit.

Garnet is a silicate mineral that is generally used as an abrasive. Given it is only 6 percent of the quantity it is most likely not economic. It could indicate potential wear issues during the mining phase of operations with a higher than usual rate of wear of drill bits when the deposit is drilled as part of drill and blast mining operations.

Similarly quartz would be of no economic value. Like garnet it is abrasive and it will affect equipment wear issues.

Goethite is an iron mineral, usually of minor importance. It this situation it will most likely be a waste mineral.

Rossovskyite, columbite and tantalite are the minerals of interest.

Rossovskyite contains tantalum, niobium and titanium. There is no indication of how of each metal is present and how much can be recovered overall.

Columbite contains niobium, see comments for rossovskyite.

Tantalite contains tantalum, see comments for rossovskyite.

These minerals form 83 percent of the minerals tabulated. Only 59 percent contain tantalum.

One thing that is favorable is all the minerals are oxides, there is not a mix of oxides and sulfides which would complicate metallurgical plant design and recoveries.

Having said that, one needs to know if such oxides can be recovered easily and inexpensively. Most nickel mines mine nickel sulfides, not oxides, partly because nickel sulfides are easier and cheaper to process than nickel oxides. Nickel sulfides can be extracted using flotation, whereas nickel oxides usually require autoclaves which are essentially large pressure cookers that use acid or ammonia to treat the nickel oxides.

All you have is a table of minerals and it looks promising but there is no way to assess the economic viability of such a "deposit". What you need is a table which states the amount of metal that can be sold, stated as either so many tonnes of rock containing a particular percent of each metal of interest and the associated mining and metallurgical recoveries (i.e. something like, 200 Mt @ 2% Ta with a mining recovery of 95% and a metallurgical recovery of 85%) or so many tonnes of metal recovered (i.e. 3.5 Mt of Ta, accounting for mining and metallurgical recoveries).

$\begingroup$

$\endgroup$

1

In all likelihood it has no commercial viability in Africa. The lack of infrastructure will be a very large barrier to any production. No comment on political instability. To illustrate: in about 1970 Amoco considered producing copper from vast well-defined ore bodies. (I remember pretty well because a friend got to go to Africa to verify core test results and I was envious). Amoco made detailed cost estimates.

They needed:

- A few hundred miles of railroad

- A canal or very large pipe to bring in water many miles

- A power plant for electricity (likely fueled with imported oil)

- A town, schools, hospital, and stores for workers

Then the facilities for refining and smelting the copper. The by-product cobalt would have doubled world supply, but you can never have too much cobalt. Amoco estimated it would cost a couple billion US dollars, 1970 dollars, before the first shovel of copper ore was lifted. They decided the risk was too high. The copper is still there, parts of the ore body contain 100 times more copper concentration than copper mined in the US today. But the major corporations still considered it too great a risk.

-

2$\begingroup$ It could be argued Amoco were sensibly risk averse for the times, but there's a new player in the game now, China. If China wanted that copper I'm sure it could arrange a golden handcuff "loan" so it build the infrastructure required & to acquire the copper & thereby reduce its dependence on copper producers from elsewhere. $\endgroup$– FredCommented Sep 20, 2021 at 17:06